|  |

| |

According to U.S. experts, the most terrible modern weapon that can be deployed in global conflicts are economic sanctions. Indeed, not one country in the world today that is subject to sanctions could survive unscathed. Their recovery could take years, if not decades. Although the sanctions that the EU and U.S. have applied in the first weeks after Russia′s annexation of Crimea do not look very serious, they may only be the tip of the iceberg. Experts note that Moscow will suffer far greater losses due to the outflow of Western capital resulting from the global geopolitical split.

There are several kinds of international sanctions that countries can impose against a third party that violates certain generally accepted norms. In extreme cases, sanctions may take the form of a military operation to force the country to return to the legal framework, or to the rupture of diplomatic relations with all its attendant consequences. But most often, the international community punishes a "guilty party" by applying economic sanctions such as a total ban on trade with the offending country, as was the case with Iraq and Yugoslavia. Such comprehensive measures have a serious negative impact on the economy and average citizens. For example, during the sanctions imposed on Iraq after its occupation of neighboring Kuwait, Baghdad′s currency, the Iraqi dinar, collapsed to less than 1/20th of its value against the U.S. dollar during the period 1990-1995. Iran, which has been under Western sanctions for 35 years, has suffered much more than others. In fact, the entire structure of the economy, including foreign trade and the domestic economy, has undergone significant changes, the effects of which are felt much more by ordinary Iranians than the country′s leadership. It was only as a result of the last round of collective sanctions, when Iran′s oil exports fell from 2.4 million barrels per day in 2011 to about 1 million barrels a day now, that the government "allowed" the moderate Rouhani to talk about potential concessions to the West.

Understanding the disastrous effects of the embargo for common people, the international community has changed its policy somewhat, making its sanctions more directed against specific representatives of the country. In this case, some of the political elite or business leaders involved in political processes may be faced with measures such as limiting access to foreign financial markets, freezing foreign financial assets and a ban on entry into states participating in the imposed sanctions.

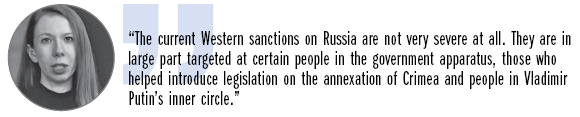

Hannah Thoburn, a fellow at the Foreign Policy Initiative, told WEJ:

Immediately after the start of economic conflict, the World Bank warned that if tougher sanctions were imposed, the Russian economy could expect a period of stagnation, if not recession. World Bank analysts have predicted two scenarios for the further development of events surrounding Crimea. If the consequences of the Crimean crisis are short-lived, and the West decides not to harm itself by imposing harsh sanctions against Moscow, then the Russian economy will grow by 1.1% this year. The second scenario is more pessimistic and takes into account the possibility that the EU and U.S. will adopt additional disincentives in the form of trade sanctions. In this case, Russia′s GDP could shrink by 1.8% for the first time in the past decade. The U.S. rating agencies S&P and Fitch immediately decided to be proactive by downgrading Russian′s long-term rating from "stable" to "negative."

According to Thoburn:

Indeed, we must not forget that Western countries themselves will suffer if tougher sanctions are imposed. And while these consequences will be quite insignificant for the U.S., they could be much more serious for the EU countries. More than half of Russia′s federal budget is funded by revenues from gas and oil exports to EU countries, so any economic sanctions associated with fossil fuels would deliver a serious blow to the federal budget. On the other hand, about 25% of the EU’s gas comes from Russia, and the energy dependence of eastern EU members in some cases is as much as 80–90%. Moreover, both Gazprom and Rosneft have close contacts with European energy companies, and the rupture in relations will impact Europeans no less than Russian companies. Therefore, if further sanctions affect the energy sector, then the EU will need to refocus its eastern members on receiving supplies from other sources, such as Norway. This process will take time and will impose an additional financial burden. After all, today Europe is not able to function normally without Russian hydrocarbons.

In any event, Russia′s relations with the West have been taken a hard hit, and Russia will have to diversify its trade flows and main channels of income. The BRICS group of countries may play an important role in this process. They condemned the sanctions imposed on Russia in a recent joint statement. Thus, Moscow′s reaction to the loss of the European market, and the oil and gas sector in particular, may represent a shift towards emerging markets, especially China. Today, China is Russia′s second largest partner after the EU in terms of the former′s imports of hydrocarbons. Twelve percent of such Chinese imports come from Russia. Despite the lower revenue from Chinese contracts and less developed infrastructure, in the future China may replace the European vector. However, it would cost Russia more money and take it more time to transfer all of its pipelines to China than Europe would require to free itself of the need for Russian oil and gas.

In fact, the formal legal sanctions may only be the tip of an iceberg that will impact the Russian economy, which has been weakening over the past year. In addition, according to experts, Crimea′s development will require approximately €3.5 billion per year from Russia, and in the medium term approximately €20 billion per year will need to be invested into the regional economy. The main problem today is the loss of confidence of Western investors. According to the World Bank, over the first quarter of this year alone investors have withdrawn $70 billion from Russia. This a sum exceeding capital outflows for all of 2013 ($63 billion). According to the Ministry of Economic Development of Russia, capital outflows from Russia in 2014 will amount to $100 billion. If a scenario develops where the political conflict with the United States worsens, outflows could reach a record $150 billion.

Text: Olga Irisova, Anton Barbashin